...und hält Pfizer für am aussichtsreichsten.

fette Hervorhebungen und der Kommentar in eckigen Klammern sind von mir.

----------------------

Is Big Pharma a Bargain?

By Charly Travers (The Motley Fool BreakerCharly)

February 22, 2005

As the drug industry analyst for Motley Fool Rule Breakers, I spend the bulk of my time looking at small-cap biotechs -- those companies with light wallets and thin pipelines that are either going to make investors a fortune or send them to the poorhouse. Sitting in the front seat of a rollercoaster is where my interests lie, and I generally don't pay much attention to the relatively stable large biotechs or big pharma companies.

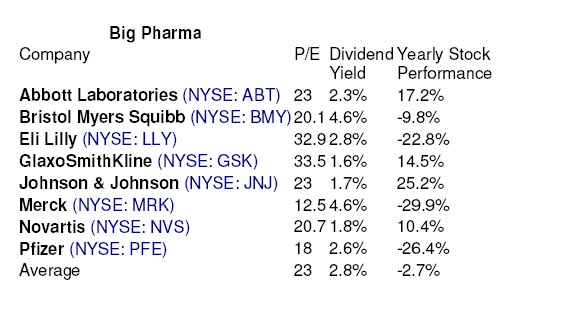

But recently, I have started to sniff around the big drug makers. For the last year or so, big pharma has been a punching bag for drug industry critics, politicians, class-action law firms, and the general public. These groups have created a few black clouds that are hanging over the industry, including drug reimportation, price controls, calls for more rigorous FDA oversight, and litigation. These concerns have made investors a bit skittish about big pharma, as you can see by the share price performances over the past 12 months in the table below:

As a whole, this group of drug companies has seen an average share price decline of 2.7% during a period in which the S&P 500 gained 5%. Because of this dismal performance, the trailing P/E ratio for the group is 23, with a dividend yield of 2.8%. For someone who is used to seeing big pharma with a P/E near 30 and a yield close to 2%, these numbers have piqued my interest.

I'm not saying these numbers mean we have a once-in-a-lifetime, no-brainer opportunity. These companies are cheap on a historical basis, but they're not making me salivate. But I do think this is a good time to pick up high-quality, dominant companies with long track records of increasing earnings and dividends.

I bet I would beat the market handily if I socked this group away in my portfolio and forgot about it for 20 to 30 years. Taking this long-term view, I'm going on the record as being bullish on big pharma. That's a first for me, and there were times I believed this day would never come. This is not to say that all of the drug industry's problems have miraculously been solved. There are some lingering issues remaining.

What about reimportation?

Drug reimportation is the bulk purchase of drugs from other countries, where government-mandated price controls keep costs low. The rationale for such an idea is that if entities, such as state health-care systems, could buy drugs from overseas, they could save a bundle of money.

I think there were until recently significant worries of this happening on a grand scale, which would cause sales and profits amongst pharmaceutical companies to plummet. For much of the past year, these concerns have been weighing down pharma stocks despite comments out of Fooldom that it wasn't going to happen. As colleague Bill Mann has pointed out, big pharma controls the supply, so it can simply choke off the flow of goods into places like Canada, leaving no drugs to be shipped back to the U.S.

As if that weren't enough, the final nail in the reimportation coffin came this past week when the Canadian health minister announced that the Canadian government is considering a total ban on the export of branded prescription drugs. This is a topic that fellow Fool Brian Gorman hit on last month, and I agree that the threat of cheap drugs flowing into the U.S. has been minimized.

Drug safety

Ever since Merck voluntarily pulled its blockbuster drug Vioxx off the market last September, there have been concerns that the FDA has been too lax in overseeing drug safety and that it needs to crack down. That's bunk. I've always found the FDA to be rigorous in reviewing drugs. However, sometimes it seems that people want drugs to be as safe as a glass of water, and that's just not going to happen. It's impossible. As the old saying goes, "Show me a drug with no side effects and I'll show you a drug that doesn't work."

Legitimate concerns about other drugs in Vioxx's class were raised and I think there were worries about whether Pfizer would catch Merck-itis. Like Vioxx, Pfizer's Celebrex and Bextra are COX-2 inhibitors that are huge blockbusters. Despite Pfizer's size, getting pinched on these drugs would hurt.

As it turns out, Pfizer is likely going to emerge from this controversy relatively unscathed -- or at least far better off than industry skeptics were predicting. Within the past few days, a FDA advisory panel met to discuss Bextra, Celebrex, and Vioxx and voted that all three should be on the market despite cardiovascular risks because, despite the potential problems, these drugs are quite helpful for certain patients.

There is a broad lesson here. The FDA is going to be reasonable with respect to weighing the benefits of a drug against its risks. For the most part, I believe the FDA has been pretty fair in this regard. So I don't think investors need to worry about the FDA enacting draconian safety measures that would cripple the drug industry.

If I had to pick just one

There are a lot of high-quality drug companies for investors to choose from right now. It is very tempting to go with Merck with its P/E of 12.5 and a dividend yield of 4.6%. That's especially true in light of the possibility that Vioxx could get back on the market, although given the black mark on this product's name, it's not likely it would return to its former sales levels. But Merck doesn't just have unquantifiable legal liabilities, it has looming patent expirations of blockbuster drugs, including the loss of Zocor in 2006. So while I don't think Merck is going to go under due to potentially large legal costs, I also don't find the situation to be terribly exciting.

Right now, I think the better bet is Pfizer. Over the past six months, Pfizer has been beaten down about 15% over the COX-2 scare. Given the recent FDA panel's vote in favor of these drugs, Pfizer is now a particularly compelling buy. Think about it: The top drug company in the world is now yours for the taking with a P/E under 20.

[Kommentar: Das 2005-KGV liegt zurzeit bei 12,5 - wobei die mittlere Analysten-Gewinnerwartung von 2,12 Dollar pro Aktie noch aus der Zeit VOR der FDA-Panel-Abstimmung stammt. Da ist der zu erwartende Umsatz-Rebound mit Celebrex also noch gar nicht eingepreist!]

Pfizer is actually cheaper on a relative basis than the rest of its peers and it doesn't have the same near-term patent problems or potential legal liabilities that Merck has. I'm also quite confident that the company will continue to get its hands on top drugs to reload its pipeline. It has been very keen to load up on big sellers through acquisitions and that trend will surely continue. Not only is Pfizer sitting on the $10 billion drug Lipitor, it goes out and buys a company like Esperion Pharmaceuticals to try to keep its dominant share of the humongous cholesterol market for the foreseeable future.

While much of the drug sector is looking pretty tasty, Pfizer, with its attractive relative valuation, dominant marketing presence, and willingness to buy up blockbuster drugs, heads the list.

|

Angehängte Grafik:

Tab.jpg (verkleinert auf 87%)

1 |

... |

5 |

6 |

7 |

|

9 |

10 |

11 |

...

| 198

1 |

... |

5 |

6 |

7 |

|

9 |

10 |

11 |

...

| 198

Thread abonnieren

Thread abonnieren