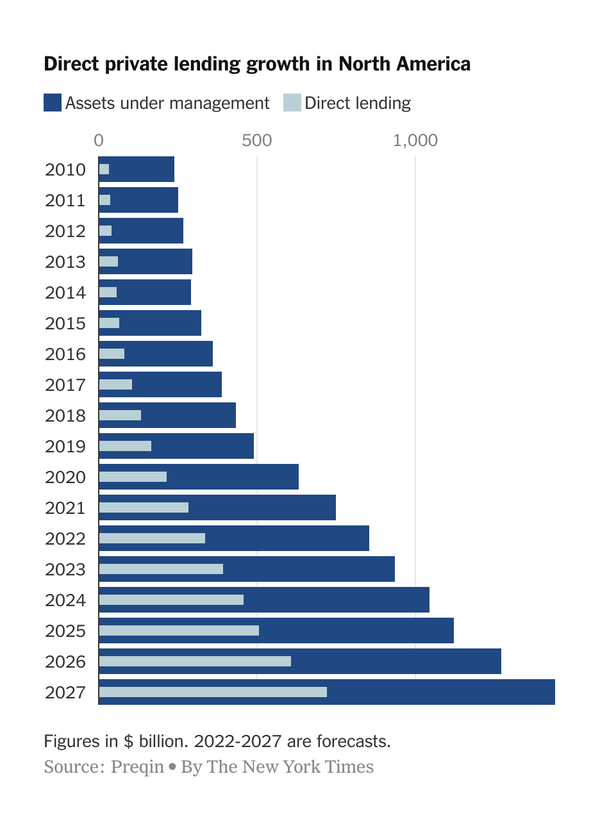

Regional Bank Turmoil Pushing More Lending to Direct Private Lending: giant investment firms like Apollo Global Management, Ares Management and Blackstone — are chomping at the bit to step into the vacuum. For the last decade, these institutions and others like them have aggressively scooped up and extended loans, helping to grow the private credit industry sixfold since 2013, to $850 billion, according to the financial data provider Preqin. https://matttopley.com/wp-content/uploads/2023/05/image-54.png https://www.nytimes.com/2023/05/06/business/...isis-shadow-banks.html

A recession and a credit crunch could result in $1 trillion of corporate debt defaults, Bank of America says: A full-blown recession and credit crunch could spur an 8% corporate default rate, BofA estimated. That would put nearly $1 trillion of existing corporate debt in distress, the bank said in a note. https://finance.yahoo.com/news/...-crunch-could-result-003636596.html

JohnLaw

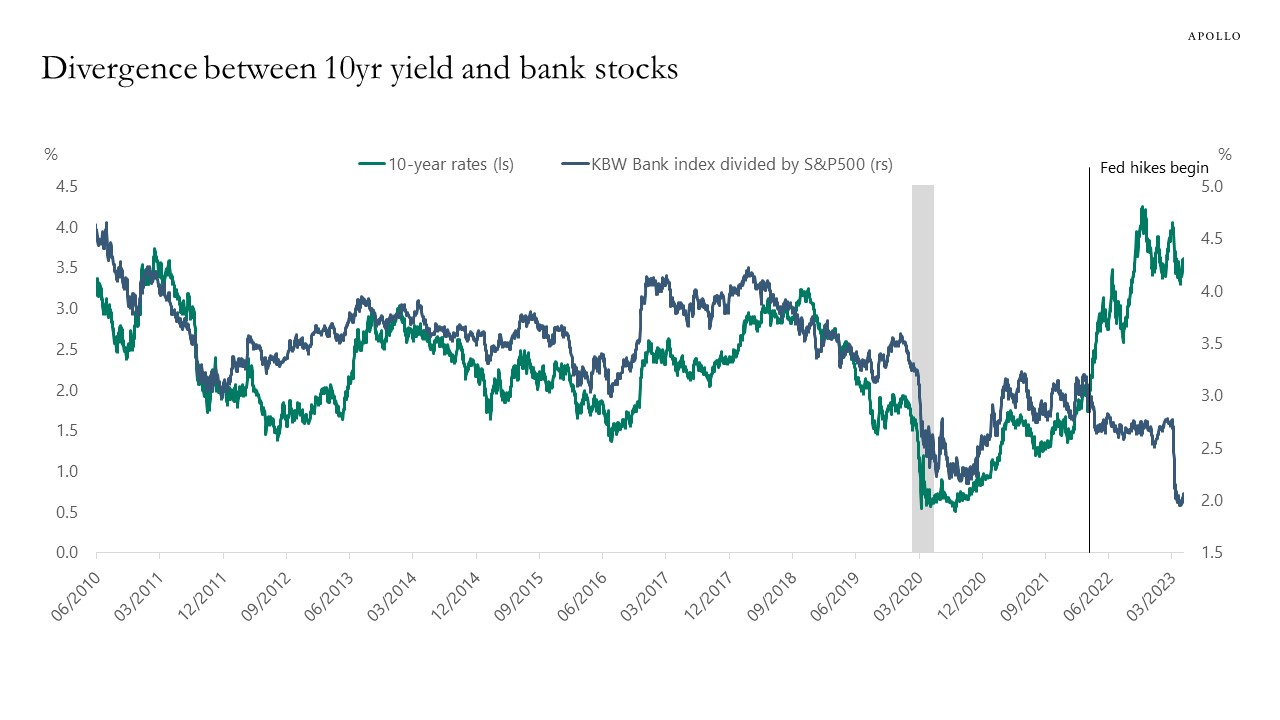

: Correlation Between Banks and 10s Breaking Down

Correlation Between Banks and 10s Breaking Down: It used to be the case that higher long-term interest rates were positive for banks because higher long rates meant wider net interest margins. But since the Fed started hiking rates last year, this correlation has broken down, see chart below. https://apolloacademy.com/wp-content/uploads/2023/...1223-Chart-1.jpg Now higher rates are negative for banks because it has a negative impact on their assets, and higher rates and an inverted yield curve increase the risks of a recession and hence credit losses. https://apolloacademy.com/...ion-between-banks-and-10s-breaking-down/

Bank Credit Conditions at 2008 Levels: In addition, the first sentence in the notes to the Fed’s Senior Loan Officer Survey shows that it only covers large banks out of the roughly 4,000 banks in the US, so credit conditions in small and medium-sized banks are likely tightening even more than seen in the charts below. https://apolloacademy.com/bank-credit-conditions-at-2008-levels/

JohnLaw

: FDIC: Special Assessment Pursuant to Systemic Risk

FDIC Board of Directors Issues a Proposed Rule on Special Assessment Pursuant to Systemic Risk Determination: he Federal Deposit Insurance Corporation (FDIC) Board of Directors today approved a notice of proposed rulemaking, which would implement a special assessment to recover the cost associated with protecting uninsured depositors following the closures of Silicon Valley Bank and Signature Bank. https://www.fdic.gov/news/press-releases/2023/pr23037.html

Latest Trilogue: SI and dark trading restrictions left to the wayside and a regional ban on PFOF retabled European Commission has also been tasked with drafting an additional tape proposal aimed at bridging the gap between opposing views put forward by the European Parliament and Council https://www.thetradenews.com/...-and-a-regional-ban-on-pfof-retabled/

Regulating payment for order flow might not work: The SEC is looking into whether a controversial practice called payment for order flow — a growing source of revenue for retail brokers and wholesalers — creates a conflict of interest. A 2021 SEC report on the retail investor mania for GameStop and other so-called meme stocks suggested that some brokerages might be profiting from PFOF at the expense of their retail customers. https://mitsloan.mit.edu/ideas-made-to-matter/...entionist-approaches

JohnLaw

: Die Banken machen denselben Fehler wie 2008

„Die Banken machen denselben Fehler wie 2008“: Der langjährige Fondsmanager André Stagge hält die Bankenkrise mitnichten für ausgestanden – im Gegenteil. Er sieht wachsende Risiken in den USA. Zumal die Banken dort in ihrer Jagd nach Rendite schon wieder auf verbriefte Kreditportfolien gesetzt haben. https://www.focus.de/finanzen/boerse/...er-wie-2008_id_193879807.html Collateralized loan obligations deliver worst returns in years :(Bloomberg) --The $1.3 trillion market for reselling leveraged loans is facing its lowest profitability in years, potentially making it harder for lower-rated companies to refinance debt. The collateralized loan obligation market — the biggest buyer of leveraged loans — is getting squeezed as funding costs rise relative to the returns on investments. https://asreport.americanbanker.com/articles/...orst-returns-in-years Fed’s $2.6T MBS dilemma – rising rates could trigger massive portfolio losses: Delve into the complex world of mortgage-backed securities (MBS) and the Federal Reserve’s $2.6 trillion holdings. As interest and mortgage rates rise, the value of these securities is at risk of a substantial decline… https://cryptoslate.com/insights/...trigger-massive-portfolio-losses/ Fannie Mae Announces Rescission of LLPAs Based on DTI Ratio https://singlefamily.fanniemae.com/media/36061/display

Thread abonnieren

Thread abonnieren

{kind=link}

{kind=link}

{kind=link}