Amyris relaunch

Thread abonnieren

Thread abonnieren

|

--button_text--

interessant

|

|

witzig

|

|

gut analysiert

|

|

informativ

|

0

Optionen

| Antwort einfügen |

| Boardmail an "derhexer" |

|

Wertpapier:

Amyris Inc

|

0

In h o h e m B o g e n werfe ich diese Looseraktie nun aus meine Depot! Koste es was es wolle!

Ich werde nie wieder wegen irgendeiner noch so wundervollen Firma meinen Anlegergrundsätzen fern bleiben. Das war meine Lektion, die ich anhand dieser Aktie gelernt habe.

Außerdem habe ich festgestellt, dass nahezu ausnahmslos nur meine selbst recherchierten Aktien (bspw. CARDLYTICS INC. oder aktuell SMIC) gut laufen.

Ich mache drei Kreuze und fühle mich nun endlich befreit, diese Aktie losgeworden zu sein!

Mann oh Mann! Man lernt echt nie aus!

-----------

MfG bauwi

Die Freiheit des Menschen liegt nicht darin, daß er tun kann, was er will, sondern das er nicht tun muß, was er nicht will.

MfG bauwi

Die Freiheit des Menschen liegt nicht darin, daß er tun kann, was er will, sondern das er nicht tun muß, was er nicht will.

Optionen

| Antwort einfügen |

| Boardmail an "bauwi" |

|

Wertpapier:

Amyris Inc

|

1

Optionen

| Antwort einfügen |

| Boardmail an "macSteve0702" |

|

Wertpapier:

Amyris Inc

|

0

die meisten werden es schon gelesen haben, trotzdem unten nochmal die Stellungnahme von Amyris zu der Klage von Lavvan .

Wie ist eure Meinung, nachkaufen oder doch erstmal abwarten? Wenn nachkaufen, könnte es noch weiter runter gehen?

EMERYVILLE, Kalifornien, 11. September 2020 /PRNewswire/ -- Amyris, Inc. (Nasdaq: AMRS), ein führendes Unternehmen der synthetischen Biotechnologie auf den Märkten für saubere Gesundheit und Schönheit durch seine Verbrauchermarken und ein Top-Anbieter von nachhaltigen und natürlichen Inhaltsstoffen, reagiert auf die Pressemitteilung von LAVVAN, Inc. (LAVVAN) im Zusammenhang mit der Einleitung einer Klage gegen Amyris, Inc. (Amyris) wegen Patentverletzung und Veruntreuung von Geschäftsgeheimnissen am Donnerstag, den 10. September 2020.

Amyris und LAVVAN schlossen im März 2019 eine Forschungs-, Kooperations- und Lizenzvereinbarung ("RCL-Vereinbarung") im Wert von 300 Millionen US-Dollar in Form von Meilensteinzahlungen, die von LAVVAN an Amyris zu leisten sind, zusammen mit einer Lizenzvereinbarung, die auf LAVVANs kommerziellen Verkäufen von designierten biosynthetischen Cannabinoiden basiert. LAVVAN leistete 2019 eine einmalige Zahlung von 10 Millionen USD für die Lieferung des ersten technischen Meilensteins.

Amyris möchte die folgenden Punkte klären:

1. weiterhin F&E-Ressourcen für das LAVVAN-Programm bereitstellen: Amyris hat seine F&E-Ressourcen in Übereinstimmung mit dem RCL-Abkommen seit Beginn des Kooperationsprogramms mit LAVVAN eingesetzt und weiterhin auf die Ergebnisse der Zusammenarbeit bis 2020 hingearbeitet.

2 Der ausgeschlossene Markt: Das RCL-Abkommen erlaubt Amyris, seine Entwicklungs- und Kommerzialisierungsbemühungen in Bezug auf Cannabinoide auf dem ausgeschlossenen Markt, wie er im RCL-Abkommen definiert ist, durchzuführen. Amyris wird weiterhin seine Rechte ausüben, um innerhalb der Grenzen des RCL-Abkommens einzigartige biosynthetische Lösungen auf den Markt zu bringen. Amyris wird das RCL-Abkommen in seiner geänderten Fassung heute auf einem Formular 8-K der Öffentlichkeit zugänglich machen.

3.2020 Umsatzerwartung nicht betroffen: Amyris hat seine Umsatzerlöserwartung für 2020 durch eine deutliche Reduzierung der aus dem RCL-Abkommen erwarteten Einnahmen aus der Zusammenarbeit gesenkt. Dementsprechend erwartet Amyris keine durch das RCL-Abkommen verursachte negative Auswirkung auf die Einnahmen für die Bilanz des Jahres.

"Bei Amyris haben wir die führende Plattform für synthetische Biologie aufgebaut und durch strategische Kooperationen und Partnerschaften mit einigen der weltweit führenden Unternehmen die erfolgreiche Kommerzialisierung von acht unserer zehn Fermentationsmoleküle im Maßstab 1:1 erreicht", sagte John Melo, Präsident und Chief Executive Officer. "Im Laufe der Jahre haben wir aus diesen Partnerschaften Einnahmen von mehr als 650 Millionen US-Dollar erzielt. Amyris ist enttäuscht, dass LAVVAN den öffentlichen Bereich gewählt hat, um seine Position zu artikulieren. Amyris hat das RCL-Abkommen mit LAVVAN nicht gebrochen, und wir werden weiterhin in Übereinstimmung mit seinen Bedingungen arbeiten. Wir werden unsere gesetzlichen Rechte so weit wie möglich wahrnehmen, einschließlich einer energischen Verteidigung gegen jegliche Behauptungen von LAVVAN".

Optionen

| Antwort einfügen |

| Boardmail an "Sareim" |

|

Wertpapier:

Amyris Inc

|

2

- Lavvan - man ist sich keiner Verfehlung bewusst, alle Vertragspunkte wurden eingehalten. Das man in bestimmten Märkten selbst aktiv werden

darf ist vertraglich festgehalten

- Alleine im Cannabinoids sieht 1,5 Mrd. Dollar Potenzial

- Man ist weiter optimistisch im 4. Quartal profitabel zu werden

Optionen

| Antwort einfügen |

| Boardmail an "macSteve0702" |

|

Wertpapier:

Amyris Inc

|

Angehängte Grafik:

praeamyr.jpg (verkleinert auf 89%)

praeamyr.jpg (verkleinert auf 89%)

0

Optionen

| Antwort einfügen |

| Boardmail an "Hatti" |

|

Wertpapier:

Amyris Inc

|

0

https://www.stocktitan.net/news/AMRS/...approval-by-f02jqqwn4w36.html

Optionen

| Antwort einfügen |

| Boardmail an "NiklasJB" |

|

Wertpapier:

Amyris Inc

|

0

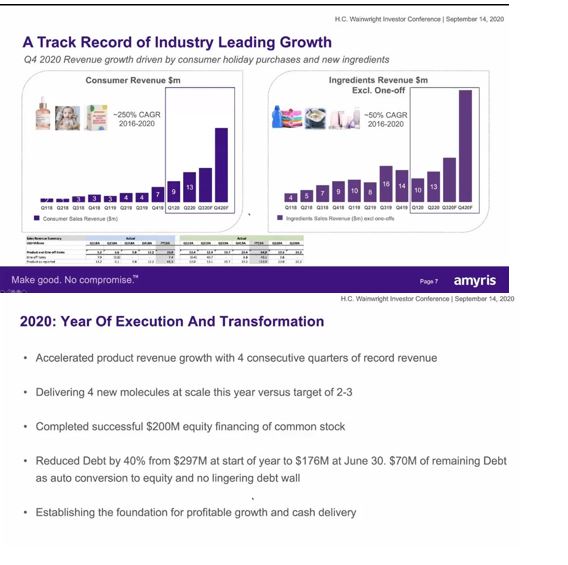

die Präsentation, auf die macsteve schon hingewiesen hat, ist lesenswert - wobei dem Grunde nichts neues dabei ist. Gut ist, dass man an allen forecasts festhält. Hier kann man die selbst lesen: https://investors.amyris.com/events-and-presentations

Bei der Präsentation (die ich selbst nicht gehört habe) scheinen noch andere interessante Dinge gesagt worden zu sein: Man hat dieses jahr 4 vermarktungsreife Neuprodukte. Wie Industrial Biotec Indes twittert, sind dies Vanillie, humane Milch-Glykane (das ist der Hammer!), ein Adjuvant (ist ja bereits bekannt) und Antikörper (das ist ebenfalls der Hammer - hier soll wohl auch noch eine Kooperation bekannt gegeben werden - wobei man nach Lavvan ja erstmal die Schnautze voll hat.). Hier das Twitterzitat: "But first of all, new products on the way this year #Vanilla #HMO #Adjuvant #Antibodies from $AMRS"

Aus den Boards erfährt man außerdem von den Zuhörern, dass wohl noch ein Molekül verkauft werden soll im zweiten Halbjahr. Letztlich geht das wohl auch nicht richtig viel anders - Selbstvermarktung ist einfach ein stück arbeit - und das letzte Vitamin hat über die Jahre 150 Mio Fees gebracht.

Dem Lavvan Ding sieht man wohl sehr entspannt entgegen - ich sehe das inzwischen auch so - wenn man sich überlegt, dass sich die Verwerfungen seit April abzeichnen und Doerr danach noch ordentlich investiert hat. Dem traue ich irgendwie.

Optionen

| Antwort einfügen |

| Boardmail an "derhexer" |

|

Wertpapier:

Amyris Inc

|

0

Optionen

| Antwort einfügen |

| Boardmail an "derhexer" |

|

Wertpapier:

Amyris Inc

|

0

...dass lavvan möglicherweise so eine halbe briefkastenfirma ist/war. Da damit verbundene Frage, warum Melo das nicht gesehen hat, wird ausgeblendet.

...dass die firma, die die anklage gebastelt hat, eine start-up ist ... die auch eher solche lawsuits streuen, in der hoffnung, dass ein einzelnes verfängt. (melo hat rausgehauen - am 14ten - dass die anwälte von amyris hier vollkommen entspannt sind)

wie dem auch sei - die umsatzprognose schein ohne die lavvan zahlungen bestand zu haben - und das ist gut - weil lavvan in der vergangenheit DER unsicherheitsfaktor war - ich sehe demnächst wieder kurse deutlich über drei dollar...

Optionen

| Antwort einfügen |

| Boardmail an "derhexer" |

|

Wertpapier:

Amyris Inc

|

0

aber - der markt ist ja auch insgesamt schwierig - spannend wird es werden ob amyris nächste woche noch eine ausführliche Antwort auf den lawsuit gibt.... frist von 21 Tagen ist dann vorbei. wenn da selbstbewusst und klar kommuniziert wird, könnte das etwas ruhe geben - könnte.

rechne in den nächsten wochen mit einer meldung zu vanilla und der kooperation mit den antikörpern - sonst hätte melo das nicht schon so rausgehauen. ob the die lizensierung melden, hängt sicher von der höhe ab. hoffen wir mal auf einen guten abschluss - dann wird dieses Phantasma weiterer Verwässerung aus dem Markt genommen.

Optionen

| Antwort einfügen |

| Boardmail an "derhexer" |

|

Wertpapier:

Amyris Inc

|

0

aber wenn sich solche betrachtungen durchsetzen - und squalane mal richtig geordert wird ... das wäre schon ein richtiger befreiungsschlag - wenn nur das wörtchen wenn nicht wäre...

Optionen

| Antwort einfügen |

| Boardmail an "derhexer" |

|

Wertpapier:

Amyris Inc

|

0

hier wird auch davon gesprochen, dass man an alternativen arbeitet - auf eben jener sugarcane basis, die amyris vertritt. Amyris wird zwar nicht explizit erwähnt - aber in einer PR wurde ja kürzlich verkündet, dass man im spiel sei. das wäre natürlich ein riesending.

das ist schon wesentlich - und das argument denkbar einfach: ein aus wildtieren gewonnener rohstoff kann nicht nachhaltig sein.

Optionen

| Antwort einfügen |

| Boardmail an "derhexer" |

|

Wertpapier:

Amyris Inc

|

0

... und alles keine pommesbuden ... leider nur halbe artikel - habe keinen bock mich auf dreitausend protalen anzumelden ...

Optionen

| Antwort einfügen |

| Boardmail an "derhexer" |

|

Wertpapier:

Amyris Inc

|

Angehängte Grafik:

original_246652447.jpg (verkleinert auf 79%)

original_246652447.jpg (verkleinert auf 79%)

1

Optionen

| Antwort einfügen |

| Boardmail an "derhexer" |

|

Wertpapier:

Amyris Inc

|

Angehängte Grafik:

ohne.jpg (verkleinert auf 51%)

ohne.jpg (verkleinert auf 51%)

2

unter

https://www.techtimes.com/articles/252900/...round-500-000-sharks.htm

heißt es im letzten drittel:

....In the petition, Shark Allies says that while shark liver oil commonly used because it is cheap to create, there are 'better alternatives' to produce squalene. Thus, they urge regulatory agencies and pharmaceutical companies to find shark squalene replacements that are not extracted from animals.

The group also urges them to develop and support the large-scale production of non-animal squalene as well as to include this new oil in testing for current and future products.

A Silicon Valley-based company Amyris is among the producers of squalene derived from sugarcane. The company said in a statement that it can produce enough oil for one billion vaccines in one month or less, although its synthetic squalene has not yet received approval for vaccine use.

Amyris Chief Executive John Melo said he is currently meeting with U.S. regulators to allow their squalene to be used as an adjuvant in vaccines to replace the shark-based squalene....

Optionen

| Antwort einfügen |

| Boardmail an "derhexer" |

|

Wertpapier:

Amyris Inc

|

1

https://seekingalpha.com/article/...flow-earnings-and-70-year-returns

alles im lot:

Amyris On Track For Cash Flow, Earnings And 70%/Year Returns

Sep. 29, 2020 2:38 PM ET|9 comments | About: Amyris, Inc. (AMRS)

Graham Tanaka

Graham Tanaka

Growth, Registered Investment Advisor, mutual fund manager, Tech

(224 followers)

Summary

Amyris bolsters balance sheet, shifting focus to cash flow, 40-50% revenue growth and earnings (we estimate $0.72 EPS in 2024).

Amyris' Q2 revenues came in light, but management adopted a more conservative philosophy and still reiterated positive Q4 EBITDA.

Amyris enhances recurring revenues with new products for Biossance, Pipette, Flavors, Clean Silica, PureCane, and surprisingly, a cannabinoid.

CBG and other extra-high value/low cost new products could disrupt billion-dollar markets and add revenue and EPS upside to our model.

New products would also add upside to our $21.60/share target in 2024 which already implies 70%/year returns.

Amyris is on a path to positive cash flow, 40-50% revenue growth and strong earnings in 2021-24

With a more stable balance sheet, Amyris (AMRS) ($2.53) is in a better position to continue to grow its current Consumer product lines 100%/year, grow its Ingredients businesses 40-50%/year and maximize its R&D pipeline to drive additional growth for many years to come.

On the strength of rapid revenue growth and 40-65% gross margins, Amyris will soon reach positive EBITDA, positive earnings and then rapid 50-100% earnings growth.

Through its financially difficult times, Amyris continued to invest heavily in its science. The result is an industry-leading platform of intellectual property and expertise in engineering yeast strains and in advanced fermentation that have enabled Amyris to successfully commercialize an industry-leading 10 molecules.

Amyris' mastery of the craft has enabled it to deliver superior products (higher purity) at lower costs than traditional production methods, allowing Amyris to enter new markets, rapidly gain market share and earn high margins.

Better science has allowed Amyris to build successful, fast growing Consumer brands from scratch (B to C) and build strong B to B partnerships with leading multinational brands.

Amyris' recent track record gives me confidence it can repeat these successes entering new and diverse markets in the years ahead.

We present our earnings model which we believe conservatively shows how Amyris will grow its revenues much faster than its operating costs. The natural result is that once Amyris passes breakeven, its high margins will help grow earnings disproportionately faster than revenues.

Our 2024 EPS estimate is $0.72 fully taxed and fully diluted, from which we arrive at our target price of $21.60/share in 2024 based on a 30 times P/E, for potentially a 70%/year compound return.

We should note that our model is based on our forecasts for Amyris to continue to gain share with its existing products. Any new products introduced in subsequent years would add upside to our estimates.

Q2 revenues came in light, but the real story is management's more conservative posture on guidance

On August 6th, Amyris reported revenues of $30 million vs. analyst estimates of $35.7 million, initiating a decline of 34% in its share price from $4.94 to $3.26.

Of the shortfall, management reported $2.7 million was due to COVID-delayed startup of production by a contract manufacturer in Italy and timing of collaboration fees for $2 million, with both expected in the 2nd half.

Management also sounded conservative on H2 guidance citing the potential for COVID-19 effects on H2 financials, contributing to analysts reducing full-year revenue estimates. Opco reduced its 2020 estimate from $219.5 to $185.0 million and H.C. Wainwright from $221.7 to $182.5 million.

Yet management kept its 2020 revenue guidance of $220 million. Why? We believe management has truly adopted a more conservative philosophy on guidance and wanted to lower expectations to be able to meet or beat every quarter. We and others lowered our sales estimates accordingly. However, Amyris management must believe it could still meet the original $220 million revenue guidance if it does an asset sale or collaboration deal or receives large vaccine adjuvant or cannabinoid orders.

With greater confidence from a better balance sheet, the arrival of a new CFO, Han Kieftenbeld, with multinational public company experience and a growing base of recurring revenues, it appears Amyris is finally in a position to become conservative.

To be clear, by managing expectations lower, Amyris would appear to be taking a step backwards but is actually taking an important step forward to achieve better stock price performance and lower volatility ahead.

$200 million equity raise fixes balance sheet, provides growth capital and opens the R&D pipeline spigot

On June 4th, Amyris completed an important $200 million equity raise. Amyris used the proceeds to pay down $62 million of debt and reduced interest rates from 12% to 8-9%, making it easier to achieve positive cash flow.

While the $200 million cash raise was criticized by some as being too dilutive, an overfunding does provide "growth capital" for Amyris to pursue its many long-term product opportunities and puts the company in a stronger negotiating posture on any future asset sales, partnering deals and plant financings.

Amyris expects to be cash flow positive in Q4 2020 and analysts expect real GAAP profits by Q4 2021. This is critical, because a company can have the best new products in the world, but it can't do much with them if it doesn't have a clear path to profitability. If Amyris can generate more profit, it doesn't have to sell part of its pipeline to fund growth and can retain more value for shareholders.

Now that Amyris is close to reaching positive cash flow, it is positioned to open the spigot and commercialize more new molecules that have been brewing in its R&D labs. Can't wait to see what's next.

Amyris adds new products to its Recurring Revenues

It is not easy to keep growing consumer brands by over 100%/year especially in a COVID environment, but Amyris continues to add new products such as a new sun protection lotion to its Biossance clean beauty line of skin care products. We wouldn't be surprised to see a men's line, hair care and deodorants, all very large existing markets.

The Pipette line of baby care and family friendly products added a hand sanitizer with Squalane which is a natural moisturizer. It has met with strong demand since its March 26th launch. Pipette recently added moisturized hand wash and hand lotion products. On May 21, 2020, Pipette announced a new talc free "Baby Cream-to-Powder" product aiming to fill the void abandoned by Johnson & Johnson (NYSE:JNJ) due to the baby powder lawsuits over asbestos in their talc.

PureCane - Amyris' 3rd and newest consumer brand is virtually sold out of its no-calorie naturally derived sweetener until next year. On June 22nd, Amyris signed a multi-year agreement with AB Mauri, a leading commercial baker which could lead to low calorie hamburger buns at major fast food chains and bread at supermarkets in 2021. Our blind taste test confirmed no-calorie PureCane in tea has the same sweet taste of sugar, but without the bitter after-taste of Truvia stevia leaf Reb M sweetener and without the overly sweet saccharine taste of Sweet n' Low.

On July 15th, Amyris announced "Clean Silica," a new non-fermentation derived silica to supply the $68 billion color cosmetics industry with a more pure and better performing silica made from recycling sugarcane ashes. This should deliver revenues in 2021.

A new flavor ingredient is being introduced but was delayed by COVID from Q3 to Q4. It is believed by some to be vanilla, which would be an attractive market with high prices.

One might say these are mere line extensions, but a bigger picture view is that Amyris continues to add better performing products from its deep science-based platform to address large already existing markets. Offering better products to large markets improves the odds of successful line extensions. As Biossance and Pipette reach critical mass, thanks to economies of scale and negative working capital from online ordering, better gross margins will show up on the bottom line as incrementally widening after tax margins and higher returns on capital.

PureCane No-calorie Sweetener has significant possible upside in 2021-2024

There is rising awareness of obesity from sugar consumption and sugary soft drinks as discussed in a SynBioBeta article on the obesity epidemic in the U.S.

Obesity.png (960×656)

SOURCE: SynBioBeta: "There's A New Fermented Zero Calorie Sugar" June 21, 2020

I expect more major bakeries, food and beverage companies to adopt PureCane to remove calories but retain sugary taste. This could boost PureCane's recurring revenue and earnings upside over the next 2-3 years.

Revenues could start earlier from the beverage companies, perhaps in 2021, as governments scramble to raise tax revenues to cover their COVID-19 budget deficits. Like cigarettes, taxes on sugar-loaded soft drinks would reduce healthcare costs and improve health (reducing diabetes and cardiovascular disease).

Amyris will be adding significant new lower cost sweetener capacity next year from greater yields on its Second Generation Reb M yeast strain.

Recall from my prior May 29, 2020 Seeking Alpha article, "Why Amyris Could Be the Next Tesla," that much like Moore's Law for semiconductors, existing Amyris products should benefit from greater yields, lower costs and higher margins with each successive yeast strain.

Disruptive "Higher Value/Lower Cost" Products should provide margin upside

Some of Amyris' most recently announced new products should deliver more than the normal value and cost benefits to consumers versus competing products already on the market. These new products should showcase the value of Amyris' proprietary processes which by producing significantly higher value/lower cost products can enhance company margins going forward.

Amyris has already demonstrated it can enter diverse consumer markets and take share fairly quickly due to the superiority of its products, to wit Biossance, Pipette and now PureCane. In my experience, this is not easy and highly unusual to see a science-based company batting 3 for 3 on its first three consumer launches. Can it be repeated?

These launches have been greatly aided by Amyris' engineered yeast-based designs and fermentation processes that can inherently produce molecules that are naturally sourced, yet more pure and therefore superior to the same molecules found in nature. Custom yeast strains are designed to produce one molecule, the one you want, not several molecules that have to be separated and extracted as currently done with products that are sourced from farm grown plants or animals at great expense and retaining impurities. The single molecule focus reduces costs significantly.

Consumers ascribe higher value to greater purity which should accommodate a premium price in the marketplace. Along with lower production costs, Amyris should be able to enhance its margins significantly.

Amyris also has the option to deliver these new products at such attractive price discounts that it can take larger market shares fairly quickly. My guess is they will do a little of both and launch with margins higher than the company's average and at lower prices than current competitors. Cannabinoids may well be the first of these disruptive higher value/lower cost product opportunities.

Amyris enters multi-billion Dollar cannabinoid market

The cannabinoid industry is large with CBD used by 14% of Americans and the best known of over 100 cannabinoids. By early this year, Amyris had broken the code and delivered yeast fermentation-based CBD and CBG molecules to its marketing partner LAVVAN.

In 2019, LAVVAN paid its first $10 million cash payment to Amyris for meeting its first technical milestone. Investors awaited the second milestone payment and became optimistic that Amyris really could deliver 20 cannabinoid molecules and earn up to $300 million in cash milestone payments from LAVVAN.

These are big numbers because cannabinoids are a big and rapidly growing market. Cantor Fitzgerald and BDS Analytics estimate the US market for CBD alone was $4 billion in 2019. BDS forecasts the US CBD market will grow 37%/year CAGR from 2019-2024.

Amyris had already stated publicly that its yeast fermentation process could produce CBD at a significantly lower cost and greater purity vs. hemp-farmed and processed CBD as shown in their March 16, 2020 slide below:

Source: Amyris website March 16, 2020 slide

As seen at the bottom left of the slide, Paradigm Capital estimated that "Biosynthesis" fermentation like that used by Amyris can produce cannabinoids at a cost of $500-1,500/kg versus $3,000-5,000/kg cost for cannabinoids from farm grown hemp ("Outdoor Grown").

Fermentation costs that are 1/10 to 1/2 the cost of current farm grown competitors are truly disruptive and created room for both LAVVAN and Amyris to take a large share of the CBD market at attractive margins.

However, since Spring 2020, the silence on the LAVVAN partnership became deafening and analysts were advised to remove any partnership revenues from our models.

On its August 6th Q2 conference call, Amyris announced it would produce one ton of commercial cannabinoid this year for direct sales to the market (without LAVVAN) through its own Consumer brands and as Ingredients to its partners in the cosmetics and flavors & fragrances industries. Amyris made it clear that its agreement with LAVVAN had carved out these channels for Amyris and its partners to address with cannabinoids.

Amyris followed with a September 1, 2020 press release, with a surprise, saying it had started production of CBG as its first cannabinoid.

CBG is better than CBD

We were pleased that Amyris' first cannabinoid is CBG, not CBD, since CBG (Cannabigerol) is one of the rarest of over 100 cannabinoids. CBG is the precursor to other cannabinoids and comprises only 1-2% of most hemp strains versus CBD which can be more than 20% of a hemp plant.

Amyris also mentioned that CBG has better efficacy than CBD in 1/3 of current CBD topical applications. I believe CBG will be preferred by consumers for more uses once Amyris makes it more widely available.

A Forbes article discusses CBG's use in pain management, as an anti-inflammatory, an anti-bacterial, and anti-cancer agent as well as the high cost to extract it from hemp.

We expect that greater availability of CBG at lower prices from Amyris will also lead to more commercial and academic research on CBG's properties and efficacy and find even more uses to broaden the market for CBG. CEO Melo hinted at markets Amyris' CBG could address in a recent interview in Nutrition Insight where he cited CBG's better performance than CBD in topical indications for antioxidant, pain, inflammation and anti-acne applications. These suggest markets that Amyris might address first.

We believe CBG will command a higher selling price than CBD. In addition, Amyris should be able to deliver its CBG in a more pure form and at cheaper prices than farm grown CBG so should enjoy attractive gross margins, perhaps 50% initially. At scale, margins could eventually exceed the high end of the company's 60-65% gross margin range and perhaps move closer to 80% drug company margins.

One metric ton of CBG or 1,000 kg might generate about $5-10 million in revenues for Amyris based on $5-10/gram pricing for CBG isolate per Kush.com.

A campaign to produce one ton this year is an important announcement as Amyris would demonstrate it can disrupt the entire multi-billion dollar cannabinoids market with commercial lot sizes that are more pure (free of hallucinogenic THC), at a cheaper cost, more sustainably and with more economies of scale than current farm grown, hemp-derived cannabinoids.

So, while LAVVAN's inactivity has caused analysts to remove milestone payments from their models, Amyris has begun to generate its own cannabinoid revenues.

Amyris said it will produce one ton of CBG this year (in 4 months) which might imply about 4 tons/year at scale. My preliminary guess is with four CBG lines next year, they could produce 16 tons or 16,000 kg. Assuming Amyris will drive prices lower in 2021 to $4/gram, that would suggest revenues of $64 million, versus the $22.5 million revenues we have in our model. We will maintain our more conservative 2021 estimate and wait for additional information.

Assuming gross margins conservatively of 65%, sales of $64 million would deliver $41.6 million of gross profit. If pretax margins are 40%, Amyris could generate pretax profit of $25.6 million or $0.07/share pretax FD. This is not a prediction, but merely serves to illustrate the EPS leverage and upside potential that could kick in when Amyris enters large existing markets with a significantly lower cost product.

LAVVAN Surprise Lawsuit

On September 10, 2020, LAVVAN filed a lawsuit against Amyris claiming patent infringement and trade secret misappropriation. My preliminary interpretation is that LAVVAN has not been able to raise sufficient capital to pay Amyris additional milestones and appears to be trying to break the agreement.

This action caused an immediate 25% drop in Amyris' stock, down from $3.14, which seems disproportionately excessive. It does not change my views on Amyris. I expect Amyris will be able to sell significant amounts of CBG and other cannabinoids fully in accordance with the LAVVAN agreement. Amyris' lawyers have not yet responded.

When Does Amyris reach positive cash flow and positive EPS?

While the company believes it could achieve positive EBITDA by the 4th quarter of this year, we would be quick to point out that the first and second quarters of each year are seasonably the weakest quarters and the 4th quarter is the strongest. So, given its seasonality, I expect negative EBITDA Q1 and Q2 of 2021.

My firm's earnings model is summarized below, revised for more shares outstanding from the financing, the inactivity of LAVVAN, and more conservative company guidance. The net effect is to push out our revenue and EPS estimates by a year:

SOURCE: Benjamin Bratt at Tanaka Capital Management, tanaka.com

It is important to be aware this EPS model assumes full dilution from annual non-cash stock compensation and all 49.5 million warrants assumed to be exercised. This could result in $134 million of cash injected into the balance sheet at exercise prices of $2.87-5.02/share, with $38.5 million received in January/February 2021, $16.6 million in March and $9.4 million in May.

We expect Amyris to be comfortably profitable in Q4 2021 and report a slight loss of $(0.04)/share for the full year 2021. Understand that the actual number may vary based on the unpredictability of asset sales and the timing of receipt of collaboration fees. If you are like me, you will focus more on recurring revenue and profits which will be rising as a percent of total revenue and profits with each passing year.

Amyris is a potential 8-Bagger, compounding at 70%/year to 2024

Our model forecasts fully diluted, fully taxed earnings per share of $0.72 in 2024. With revenues conservatively growing by 28% and EPS by 53% in 2024, it is reasonable to apply a 30x P/E ratio suggesting a $21.60/share target price.

With the stock having dropped on the news of the LAVVAN lawsuit, the stock at $2.53 offers the potential for an 8-bagger or a gain of 753% over the next 4 years, which compounds at 70%/year.

Thereafter, high double-digit growth of existing products and a robust new product pipeline suggest continued strong double-digit revenue and EPS growth, making Amyris a viable investment for a decade or longer.

By late 2021, as operating margins widen, Amyris should begin to generate free cash flow. Our understanding is that capital expenditures will moderate for a few years following next year's $70 million ingredients plant construction which we estimate will utilize $20 million of company cash and $50 million of project financing.

Consistent with our earnings model, we estimate Adjusted EBITDA of $26 million in 2021, $129 million in 2022, $262 million in 2023 and $380 million in 2024. I would expect some cash would be used to buy back shares and improve EPS, but share reductions are not assumed in our model.

In the meantime, investors should be aware that a valuation of Biossance alone based on next year's sales is greater than the current market cap of Amyris. The acquisition of a comparable clean beauty company, Drunk Elephant, in 2019 by Shiseido for $845 million was valued at 6.5 times its estimated revenues of $120-130 million. We estimate that Biossance will have revenues of $52 million this year and $110 million next year. At 6.5 times revenues, this suggests a Biossance valuation of $338 million this year and $715 million next year vs. Amyris' current market cap of $519 million. We also expect Biossance to be nicely profitable next year due to more higher margin online sales and high incremental margins.

Risks to reaching positive cash flow, earnings, successful new product rollouts and 70%/year returns

Amyris still needs to execute and take the next big step to transition from an undercapitalized protracted startup to become a cash flow generating, high-quality revenue and earnings growth company. Above average 50-70% gross margins will make the task easier. So will the simple math of growing revenues 40-50%/year while limiting expense growth to single digits.

Near term, to meet guidance, Amyris needs to reach positive EBITDA in Q4 2020, or investors will be disappointed. We now project positive net income by Q4 2021 as do Sell Side analysts.

The LAVVAN lawsuit could linger longer and act as a drag on the stock.

COVID can cause delays and disrupt supply chains, although Eduardo Alvarez's operations have been running smoothly and continuously increasing productivity and output.

There may be delays on new product launches as seen with the Q2 flavoring introduction.

There is always the risk of competition. We are watching cannabinoids in particular, but we believe Amyris will be "first to market" with commercial quantities.

CEO John Melo is developing multiple new strategic growth opportunities and at the same time building a team of managers to execute on their plans for growth.

With a new CFO, a complete management team is now in place to execute on these opportunities.

With a much improved balance sheet, Amyris no longer has to rely on serial convertible bond issuances and live from asset sale to asset sale.

The big question is when do investors begin to anticipate and discount the next milestones of positive cash flow and profitability as well as potentially important news flow and upside on new products?

Investors will want to own Amyris before LAVVAN suit is settled, it beats guidance and shows more new products

Over the next 12 months, Amyris will look like a very different company, getting close to producing real earnings, with three Consumer brands generating cash flow, with cannabinoids and at least four other new products being released from its pipeline expected to add 4th, 5th, 6th and 7th sources of recurring revenue at margins above company averages.

I will be discussing the potential upside from some of Amyris' newest growth opportunities (adjuvants, HMOs, monoclonal antibodies and vaccines) in an additional Seeking Alpha article. There will be more surprises coming out of Amyris' R&D pipeline.

Hitting their financial targets as well as news on any combination of new product surprises could trigger a bounce in Amyris' stock and short covering.

Over the next few quarters, new products could inject upside to Amyris' financials, and our earnings models may have to be adjusted upwards. The CBG example was provided to suggest how we might have to revise our expectations going forward. For now, we prefer to keep our estimates conservative and be favorably surprised.

Optionen

| Antwort einfügen |

| Boardmail an "derhexer" |

|

Wertpapier:

Amyris Inc

|

0

https://seekingalpha.com/article/...ck-article&utm_content=link-2

Optionen

| Antwort einfügen |

| Boardmail an "Hatti" |

|

Wertpapier:

Amyris Inc

|

0

ich kopiere den Text hier mal rein - weil er ja irgendwann hinter der Bezahlschranke verschwindet...

aus:

https://seekingalpha.com/article/....stck.pro&utm_medium=referral

Summary

Amyris' engineered yeast strains and advanced fermentation can produce an unlimited number of new products for billion-dollar markets.

Squalane and squalene are becoming versatile Wonder Molecules with new high value applications like vaccine adjuvants added every year.

HMOs will replicate complex sugars in mother's milk for infant formula and improved gut health, which could add $0.13 to EPS by 2024.

Amyris to produce monoclonal antibodies at significantly lower costs that could double Amyris' revenues and add $0.79 to EPS by 2024.

Though only preclinical, a more effective 2nd Gen COVID vaccine with IDRI RNA and Amyris adjuvant could add $0.90/share to EPS in 2022.

Leveraging a scientific platform to offer unbounded financial upside

"Unbounded" is defined by Oxford Languages as "having or appearing to have no limits." Amyris (AMRS) ($2.53) recently announced new product launches and has hinted at forthcoming molecules about to be launched suggesting unbounded upside for revenues and earnings. Any of these new products could cause a significant revaluation of Amyris' outlook.

Most of these newest initiatives address very large $1 billion+ existing markets growing very rapidly. Since these markets already exist, Amyris only needs to demonstrate that their new proprietary engineered yeast fermentation processes produce a superior product (more pure and consistent) or at a significantly lower cost, or both.

These markets are very large particularly compared to the company's current market cap. In the next 12 months, as Amyris demonstrates it can disrupt one market after another, the pattern and path will become more clear to investors, I believe, at much higher stock prices.

In addition, Amyris is also a rising margin story. Some of the newest products and initiatives appear to be offering even more value and at considerably lower costs than existing competitors' products. Hence, these newest products should command even higher margins than the 10 molecules Amyris is already selling on the market at attractive 40-65% gross margins.

Importance of leadership in pure and applied science

The key is in Amyris' science. While investors are beginning to become aware of the nascent but rapidly emerging field of "synthetic biology," I believe in the next 12-36 months, we will witness the emergence of a company with not only industry-leading deep scientific expertise and growing intellectual property in engineering and optimizing yeast strains, but also industry-leading skills in advanced fermentation, continuous improvement of production processes and scaling to make these molecules commercially successful.

Amyris is leveraging its lead in engineering yeast strains, advanced fermentation, biotechnology, chemistry, machine learning, and artificial intelligence to produce molecules in larger volumes, with more purity, more sustainably and at cheaper costs than that which already exist in nature in less pure form and at higher extraction costs.

The number and variety of target molecules is virtually unlimited and provides for many years or even decades of growth. Based on conversations with Amyris over the last 4 years, eventually roughly half of known molecules might be producible by synthetic biology and again very roughly, half of those might be economically attractive for methods like Amyris' engineered yeast fermentation processes.

The wraps are coming off of Amyris' R&D pipeline

After the recent $200 million financing, a major reduction in debt service costs, and with further cost reductions and operating efficiencies underway, the wraps are coming off. No longer constrained by a stressed balance sheet, we will see more new product surprises coming out of Amyris' labs. Based on the most recent announcements, these are likely to be very large revenue opportunities at higher than normal margins.

The first large new product that begins to add high profit revenues could initiate a rebound in Amyris' stock which has been beaten down by the disappointing Q2 revenues and what I believe is a frivolous lawsuit by LAVVAN.

It might be CBG as discussed in my prior Seeking Alpha article, "Amyris On Track for Cash Flow, Earnings and 70%/yr. Returns." Or it might be from news flow on new applications for flagship Squalane or squalene molecules, squalene vaccine adjuvants, HMOs, monoclonal antibodies, a 2nd Gen RNA COVID-19 vaccine - or other brand new molecules to emerge from Amyris' R&D pipeline.

Squalane and squalene find many diverse applications

Every year Amyris seems to announce a brand new application of its existing Squalane and squalene molecules for a wide variety of very different markets. These are becoming Wonder Molecules due to their versatility, their own performance and their ability to enhance the performance and reduce cost of other molecules.

Squalene appears in nature as a natural moisturizer in humans, but our bodies start producing less as we get to our upper 20s in age. It is also produced by sharks and can represent 80% of shark livers. Cosmetics companies discovered the enormous benefit to maintain smooth and youthful skin and added shark squalene to their lotions but only at about 2% of volume due to the high cost to extract shark squalene.

Amyris' scientists were able to create a sister molecule, Squalane, which performs exactly like squalene except it is tweaked to extend its shelf life. Due to its efficient engineered yeast fermentation processes, Amyris can produce Squalane in a very pure form, at a much lower cost and in much greater supply than shark-based squalene. Amyris quite successfully introduced it to major cosmetics companies who are now using Amyris' Squalane in higher concentrations. The graph below shows Squalane's superior performance.

SOURCE: Amyris Neossance website aprinnova.com

Amyris has also launched its very successful Biossance skin care and Pipette baby care lines with Squalane as the key moisturizing ingredient. These Amyris brands are able to deliver better moisturizing performance shown above by utilizing more of its Squalane ingredient.

In our May 29, 2020 Seeking Alpha article, "Why Amyris Could Be The Next Tesla," we discussed Amyris' discovery that Squalane is also highly effective as a carrier oil to improve the delivery of CBD to the epidermis by 10-40 times and with much quicker absorption than jojoba and other oils.

More importantly, Amyris will likely discover many other skin supplements, ointments and therapeutic treatments whose absorption can be improved by using Squalane as a carrier, again entering large existing markets with a superior product.

Squalene as a superior adjuvant for vaccines

Amyris also developed an engineered yeast to produce sugarcane-based squalene, and on the March 12, 2020 Q4 conference call, CEO John Melo described their research into the use of this sugarcane based squalene as substitute for the shark-based squalene adjuvant for delivering vaccines. He said, "It's almost the same example that we discovered that Squalane is the best carrier oil for CBD. Think of squalene as the best carrier for vaccines to the human body."

The following generic graph from a GSK Vaccines presentation shows the theoretical benefits of an adjuvant for a vaccine's efficacy by providing an earlier and stronger immune response as well as a broader and longer lasting immune protection.

SOURCE: GSK Vaccines at Bio Conference February 7, 2018

In the 2019 Q4 conference call on March 12, 2020, CEO Melo said, "Squalene... is one of the best-performing adjuvants you can use in delivering a vaccine [but] is limited in its use due to its... being animal sourced. Shark-sourced squalene is also expensive. Sugarcane-based squalene can be 80% lower cost and can be made in unlimited quantities when needed."

The last comment is critical as shark-sourced squalene adjuvant is starting to become in short supply. Given the need for billions of vaccine shots for COVID-19 vaccine candidates superimposed on the production of normal flu vaccine shots, we would not be surprised to see strong demand for Amyris' sugarcane-based squalene as an adjuvant.

Amyris is already in discussions with three pharmaceutical companies (two are large) to provide its squalene as a low cost, more efficacious and scalable adjuvant for annual flu and COVID-19 vaccines.

In terms of timing, on the 2020 Q2 conference call, Amyris said it is negotiating the first contract for the adjuvant, and expects to have 2-3 agreements in place by year-end, of which the first could have commercial revenue before the end of the year.

Our model as shown in my prior Seeking Alpha article assumes $10 million in adjuvant revenues from one contract in 2020 which we suspect is for a Major Pharma's annual flu vaccine. For 2021, we are conservatively assuming $24 million in squalene adjuvant revenues for seasonal flu and COVID vaccines.

On the Q2 call, CEO Melo also said their profit margins on sugarcane-based squalene is double that of Squalane margins despite pricing their squalene 80% below shark-based squalene. Do the math and you can come up with decent upside potential to earnings and cash flow.

You also have to wonder why Amyris doesn't have more pharmaceutical companies trying to line up adjuvant supply moving into 2021 when COVID vaccines will really begin to increase production. There are only so many sharks, and given its available capacity, Amyris could become the only supplier left standing, creating potential near-term upside.

HMOs could start contributing higher value products next year

We have heard little from Amyris on its HMOs (Human Milk Oligosaccharides) except that Amyris has referred publicly to HMOs as a near-term revenue generator.

HMOs comprise over 200 complex sugar molecules found in mother's milk and represent a large opportunity to add these beneficial molecules to infant formula. The global infant formula market was reported by Fortune Business Insights as $45 billion in 2018 and is anticipated to surpass $103 billion by 2026.

Given the large market size for infant formula, I would make very preliminary, rough estimates that in 4 years, Amyris could be selling to its HMO ingredients partners about $200 million in HMOs/year. This could result in pretax profits of around 30%, or if licensed, about the same 30% royalty rate. This could produce $60 million per year of pretax profits equal to roughly $0.17/share or $0.13/share fully taxed. We need to hear more from Amyris on when they could initiate sales of new HMO family of molecules which we assume is sometime in 2021.

In addition, state of the art research is being done on the benefits of HMOs for improving the microbiome in the stomach in both the West and in China. We should hear more from Amyris on this second very large HMO opportunity in the next 12 months.

Contract manufacturing of monoclonal antibodies represents a very large opportunity

I debated whether to mention Amyris' research on manufacturing monoclonal antibodies because I thought it was a few years away. However, a patent was recently filed by Amyris suggesting its research over the last few years was getting ready for prime time. The timing is fortuitous as the market opportunity is getting quite large and monoclonals are notoriously costly to produce.

Then at a webcast HC Wainwright investor conference on September 14, 2020, CEO Melo mentioned that Amyris feels comfortable in its ability to build antibodies using its technology and expects to begin production in the next 6 months, scaled within the next year. This was a surprise and much earlier than we had assumed.

However, it is still very preliminary and we need to see proof of concept that monoclonals can be produced for specific target antibodies. Yet the science looks right based on the patent filing, so investors should consider its potential as the opportunity is quite large.

Fortune Business Insights estimates that the monoclonal antibodies therapy market will reach $350 billion in 2027 from $123 billion in 2019. Monoclonals represented 7 of the top 10 drugs globally in 2017, and in 2018 the top 5 monoclonals were Humira ($19.9 billion in 2018), Keytruda ($7.1 billion), Herceptin ($7.0), Avastin ($6.9) and Opdivo ($6.7).

A 2016 article in Nature America reflects Amyris' early work in providing Biogen (NASDAQ:BIIB) with its "automated strain-engineering system" to produce recombinant proteins/monoclonal antibodies more efficiently.

The opportunity is being created by the ability of Amyris' scientists to design engineered yeast strains to produce monoclonal antibodies at a much cheaper cost given the requirement for only 1/10 the capital equipment costs, quicker design cycle times and much faster production times than the biopharma industry's traditional methods.

Today, monoclonals are produced by using CHO (Chinese Hamster Ovary) mammalian cell lines that are notoriously difficult and expensive to manufacture as referenced in a recent NY Times article on a new Lilly COVID monoclonal.

On page two of its August 20, 2020 patent filing, Amyris states that their particular yeast based production line took only 2 weeks to engineer a strain vs. 3 months for CHO engineering cycle times. That is 1/6 the time to design the yeast strain.

The Amyris yeast line also doubled the production rate of the desired antibody in "just 52 minutes" vs. 19-24 hours for CHO cell lines to double production. This means that this particular Amyris yeast strain could produce the same volume as a CHO line in 1/20 of the time for a huge productivity cost savings. Although not all strains produce at the same speeds, it is probably reasonable to assume a 10 times productivity gain.

Monoclonal contract manufacturing could double Amyris' addressable market

Contract manufacturing of monoclonals represent a very large opportunity which could more than double Amyris' TAM (total addressable market) in 4-5 years. The Amyris yeast fermentation antibody production process could be utilized to produce a large percentage of any new monoclonal antibody drugs developed in the future with Amyris as the contract manufacturer or via technical out-license.

Making a very rough assumption that Amyris as a contract manufacturer can produce a $5 billion monoclonal for a pharmaceutical company and charge about 10% of the drug's value to produce it, just one monoclonal could add $500 million/year to Amyris' total recurring revenues. Two $5 billion monoclonals could add $1 billion revenues for Amyris in 2024.

Profit margins should be fairly strong at 60-70% given the potential for the savings on capital costs, design and scale up times and increasing cell line productivity by 10-20 times. At a conservative 35% operating margin, $500 million of revenues could add $175 million/year to pretax income or $0.39/share fully taxed, fully diluted for one monoclonal. Two $5 billion monoclonals could add $1 billion of revenues to Amyris and $0.79/share, fully taxed, FD. This would more than double our $935 million estimate for revenues and our $0.72 EPS estimate for Amyris in 2024.

If Amyris is able to demonstrate proof of concept and then actually starts producing the first monoclonal successfully via yeast fermentation, with such a large cost savings, it is conceivable that several monoclonals could be produced with this lower cost fermentation process, but I must point out this process is very early and drug companies may wish to start with smaller drugs first.

These are my very rough guesses and the drug industry may take its time to embrace the idea. However, the science so far looks promising and the economic benefits are significant. These calculations are not reflected in our models.

If the Amyris technology was out-licensed to the biopharma partner, I would assume the royalty rate would be higher than the typical 4-10% range given the potential for large cost savings.

The potential for contract manufacturing of monoclonal antibodies represents another opportunity for Amyris to disrupt an existing fairly large market with a lower cost solution. It is early but should be monitored.

IDRI and Amyris partner to advance novel 2nd Gen COVID vaccine and other platform vaccines

Amyris has been working with IDRI (the Infectious Disease Research Institute) for over two years to examine the pairing of Amyris' Squalene adjuvant with IDRI's proprietary nano lipid carriers and RNA vaccine platform.

On July 27, 2020, Amyris and IDRI issued a press release announcing the signing of a binding term sheet to partner and advance IDRI's novel RNA platform for a series of vaccines beginning with a COVID-19 application.

Amyris believes the partnership can deliver a 2nd Generation vaccine for COVID that many immunologists predict will be needed in 2022 and beyond as COVID is not expected to reach herd immunity and disappear. The IDRI-Amyris partnership believes its vaccine will have significantly higher efficacy than the 40-60% efficacy expected for COVID vaccines currently being developed for late 2020 and H1 2021. This is because vaccines historically have been effective for only 40-60% of the public.

It is too early to give the odds of an IDRI/Amyris 2nd Gen adjuvanted vaccine for COVID that could be significantly more effective two years from now. However, we do point out that on the Amyris Q2 conference call on August 6, 2020, CEO Melo announced that the IDRI vaccine candidate coupled with the Amyris Squalene adjuvant can be 1,000 times more efficient than other COVID vaccines currently being developed. This means that doses can be much smaller with significantly reduced side effects, and that 1,000 more vaccine shots could be produced per kg. of vaccine which should dramatically reduce the cost per vaccination.

If the program advances, I would hope that the partnership applies for government funding of clinical trials which I assume they will request. We also will have to wait until next year for any Phase 1 trial results and until 2022 for Phase 2/3 trial results which may help provide indications of risk-adjusted net present value of their 2nd Gen vaccine. The net present value of some of the 1st Gen COVID vaccine companies are very high. Moderna's (NASDAQ:MRNA) market cap is $22 billion largely based on its one Gen 1 mRNA vaccine. Too early to handicap, but vaccines represent another high value/cost advantaged revenue opportunity for a couple years down the road.

While it is very early and fraught with the high risks of any new drug or vaccine, I should suggest that my preliminary estimates are that if the IDRI/Amyris 2nd Gen COVID vaccine is more efficacious (perhaps effective for 80% of the public instead of 50%) and is used for 2 billion people (out of 7.8 billion in the world), at $2/vaccination (low because it can use 1,000 times lower concentrations of the active vaccine), it could generate $4 billion of revenue to the pharmaceutical partner to which Amyris licenses the vaccine. If Amyris receives a 10% royalty, that could deliver $400 million of royalty profits, $1.14/share pretax or $0.90/share fully taxed to Amyris in 2022. These are not in our earnings model as it is way too early.

I should note that the partnership anticipates that the IDRI COVID-19 vaccine/Amyris adjuvant program is just the first of a series of Amyris-adjuvanted vaccines from a scalable IDRI RNA vaccine platform that may be needed for other pandemics, viruses and cancers in the future. This is another large potential market opportunity, but we need to wait for further details.

Amyris' risks

With an improving balance sheet, the next financial risk is when does Amyris achieve positive cash flow? Management has reiterated it expects to be EBITDA positive in Q4 2020, and all eyes will be focused on this milestone.

There is the risk of COVID-19 affecting plant production. I have inquired several times and been told that their plants are running smoothly with COVID safeguards in place.

With new products initiating production in the next several months, there is always the risk that one will have startup difficulties and take longer to get the process right. However, Amyris has already gone up the learning curve on 10 molecules that are in full production and I am told that each new yeast fermentation process teaches them more about how to produce even more efficiently.

There is always the risk of competition entering their markets, but my sense is that there are so many opportunities for synthetic biology to replace older traditional methods of molecule production that this may not be a big issue.

I believe there is always the risk longer term of losing focus and getting spread too thin and we will monitor this possibility over time.

Investment in science is paying off

Let me be clear. It is not just that Amyris could double or triple revenues if it can produce monoclonals as cheaply as its patent filing suggests - or that Amyris could produce with IDRI the best 2nd Gen COVID vaccine to save the world from a pandemic.

The message may really be that Amyris' heavy investments over the years in basic science (going back to Aristotle's First Principles) is finally paying off, and that Amyris is doing what nobody else has been able to do by solving some of the biggest challenges of yeast strain engineering and advanced fermentation.

We still need to see that Amyris can go from lab to proof of concept to scaling of actual volume production of their newest molecules. But they have been successful so far on their existing products and it has taken important first steps by showing how the science works.

I advise owning Amyris before positive news flow and the next surprises come out of the pipeline

I have visited the Amyris headquarters and labs 4 times and attended a Bio-disrupt Investor Day, and there is one thing that stands out. Amyris is a robust, science-based company that is quickly leveraging its scientific platform to deliver highly profitable products and generate significant cash flow and earnings very soon.

Tight financials may have made it more difficult to bring promising new products out of the lab, but what happens when Amyris generates cash? I believe that the multiple Squalane/squalene products, no-calorie sweetener, vitamins, flavors and fragrances, and its newest high-margin announcements in cannabinoids, HMOs, vaccine adjuvants and monoclonal antibodies are just the beginning.

Every yeast strain that is perfected helps build the next ones. Amyris already has 10 products on the market and is ahead of its synthetic biology competitors with real revenues and soon, real profits.

With 17 molecules under development and with an Amyris goal of launching 2-3 new molecules every year, I am confident there will be more new product surprises. Most will be addressing large already existing markets offering customers products with better performance at lower prices and commanding above average margins. The financial results should follow, offering virtually unbounded upside.

In the next few months and quarters, Amyris' news flow should be quite favorable, with positive cash flow in Q4 2020 and new product news on cannabinoids, vaccine adjuvants, HMOs and its two newest products which have the largest upside potential, monoclonal antibodies and a 2nd Gen COVID vaccine. I believe it is advisable for investors to own Amyris before the new products generate more news, revenues and earnings - and before additional surprises emerge from its pipeline.

Disclosure: I am/we are long AMRS TSLA. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: This article expresses my personal beliefs and opinions relating to the subject matter contained in the article. Other than payment from Seeking Alpha for the publication of this article, I have not been compensated by any entity, and all thoughts, opinions, conclusions and statements contained in this article are my own. Further, I have no affiliations or arrangements of any kind with any entity mentioned in this article. Finally, I have purchased shares of AMRS and TSLA for myself and for my clients in the past, and if the companies continue to perform as I expect, it is likely that I will purchase additional shares of each, both for myself and for my clients.

Optionen

| Antwort einfügen |

| Boardmail an "derhexer" |

|

Wertpapier:

Amyris Inc

|

0

https://investors.amyris.com/...accines-For-All-With-No-Sharks-Killed

die interessanteste sentenz ist die folgende:

"Amyris expects commercialization and production of its alternative squalene for adjuvants in the fourth quarter." das wäre doch mal was.

Optionen

| Antwort einfügen |

| Boardmail an "derhexer" |

|

Wertpapier:

Amyris Inc

|

0

Optionen

| Antwort einfügen |

| Boardmail an "derhexer" |

|

Wertpapier:

Amyris Inc

|

1

Ich verfolge die Analysten-Kommentare und auch die Nachrichten im Forum. Die Analysten sind extrem positiv gestimmt und verleiten einem zum Nachkauf.

Mit größter Anerkennung für die guten Informationen von Macsteve, die mich aus meinem Minus ins Plus verholfen haben, würde ich mich über seine Persönliche Einschätzung Zu Amyris freuen.

Sollte man im jetzigen Zeitpunkt bereits nachkaufen (vor allem wenn man aktuell 40 % im minus) oder auf die nächsten Quartalszahlen warten?

Hast du noch weitere Investment-Ideen?

Habe TG Therapeutics und Sunpower bereits mit plus im Depot.

Vielen Dank für die bisher geteilten Informationen.

VG aus Düsseldorf

Feyyaz

Optionen

| Antwort einfügen |

| Boardmail an "Feyyaz92" |

|

Wertpapier:

Amyris Inc

|

1

scheint mir die story intakt. es gab eine reihe wirklich guter vertriebsmeldungen (china, kanada usw), ein in aussicht gestellter großer asset verkauf und aussichtsreiche kooperationen. außerdem stehen weitere moleküle kurz vor vermarktungsreife - u.a. vanille. die flagschiffe purecane, biossance und pipette laufen wie geschnitten brot. allein das mangelnde vertrauen lässt die kurse auf diesem niveau herumdümpeln.

Optionen

| Antwort einfügen |

| Boardmail an "derhexer" |

|

Wertpapier:

Amyris Inc

|

1

https://finance.yahoo.com/news/...e-research-institute-120000447.html

die plattform scheint wirklich vielversprechend - wobei, dass ganz klar eine langzeitperspektive darstellt. aber wenn ich das richtig verstehe, der konkurrenz weit voraus.

ähnlich:

https://finance.yahoo.com/news/...opment-collaboration-133000709.html

hier geht es um eine breiter aufgestellte kooperation.

Und ein neues Patent - das ich - trotz einiger Bemühungen - einfach nicht verstehe:

https://patents.justia.com/patent/10808015

Optionen

| Antwort einfügen |

| Boardmail an "derhexer" |

|

Wertpapier:

Amyris Inc

|

0

Das einzige positive was ich den Zahlen abgewinnen kann ist, dass die Herstellungskosten für selbst produzierte Produkte geringer sind als die Umsätze hieraus. Dennoch rechne ich hier jetzt mit einem ziemlichen Kursabsturz.

Optionen

| Antwort einfügen |

| Boardmail an "Marmalo" |

|

Wertpapier:

Amyris Inc

|