Der erste Krebsimpfstoff

Thread abonnieren

Thread abonnieren

|

--button_text--

interessant

|

|

witzig

|

|

gut analysiert

|

|

informativ

|

1

Einen im Ansatz ähnlichen Beitrag dazu liefert Provenge ( 40 % Überlebensvorteil nach 3 Jahren)!

Wie soll man das nach den heutigen Maßstäben in Studien nachweisen? Da ist Dendreon schon in 2007 dran gescheitert.

......But because she believes these vaccines will work best in people who do not yet have cancer, she and UPMC researcher Robert Schoen are testing the vaccine now in patients who have precancerous polyps in their colons, to see if it prevents the onset of colorectal cancer.

While she is still a couple years away from being able to report results, Dr. Finn knows the vaccine has created a strong immune response in the patients and has had few side effects..........

The hope? "If we immunize early on, the cells that become abnormal might actually be eliminated by a strong immune response," she said.

Optionen

| Antwort einfügen |

| Boardmail an "eyeonshare" |

|

Wertpapier:

Dendreon

|

2

Überlebenszeit ohne CDX liegt im Schnitt bei 15,2 Monaten mit dem Impstoff 26 Monate. Schon beeeindruckendend. Naja will hier nicht allzu viel Werbung machen, hoffe einfach Provenge wird zugelassen, denn die Entscheidung ist wegweisend für die Industrie (Cancer Vaccines). Dendreon wird dann so auf die 52 USD springen, meiner Meinung nach. Dann wird das Geld aber auch abgezogen und fliesst in andere Unternehmen, die ähnlich Potential aufweisen. Damals als Dendreon um die 3 USD tradete interessierte sich ja mal niemand für das Unternehmen, kaum Volumen damals.

* Median survival time was 26 months (95% CI: 21.6, infinity).

* Median time-to-progression (TTP) was 14.2 months.

* Median survival in a historical matched cohort was 15.2 months (95% CI: 13.9, 20.5) (p=0.0001).

* Median TTP in the historical matched control was 7.13 months (p=0.0001).

* There were no significant adverse events reported.

Skandalös war der 28.4.2010 (Dendreon)

http://www.ariva.de/...estern_nur_los_t283343?pnr=5759482#jump5759482

Optionen

| Antwort einfügen |

| Boardmail an "Andreano" |

|

Wertpapier:

Dendreon

|

0

Ich war schon auf der Homepage von Celldex aber mich würde interessieren wieviele Patienten in Phase II diese hervorragenden Ergebnisse hervorbrachten, je mehr desto besser, je weniger Patienten ums weniger aussagefähig sind die Ergebnisse, hast Du da Genaueres?

Optionen

| Antwort einfügen |

| Boardmail an "Magnetfeldfredy" |

|

Wertpapier:

Dendreon

|

1

Der Vorteil liegt hier, daß es sich um ein Medizintechnikunternehmen handelt daß nur Phase I + II zu durchlaufen hat und von den Behandlungskosten viel günstiger eingeschätzt wird als die Immunkrebstherapie!

Optionen

| Antwort einfügen |

| Boardmail an "Magnetfeldfredy" |

|

Wertpapier:

Dendreon

|

2

This study is ongoing, but not recruiting participants.

First Received: April 10, 2007 Last Updated: March 15, 2010 History of Changes

Primary Outcome Measures:

Progression-free survival status [ Time Frame: 5.5mo ] [ Designated as safety issue: No ]

Secondary Outcome Measures:

Establish the safety and tolerability profile(s) of the CDX-110 vaccination schedule in these patients. [ Time Frame: 2 years ] [ Designated as safety issue: Yes ]

Assess humoral and cellular immune responses to CDX-110 vaccinations and explore the overall immunogenicity of the vaccine as well as any interactions with steroid dosing and maintenance temozolomide. [ Time Frame: 2 years ] [ Designated as safety issue: No ]

Assess overall survival. [ Time Frame: indeterminate ] [ Designated as safety issue: No ]

Estimated Enrollment: 82

Study Start Date: August 2007

Estimated Study Completion Date: November 2010

Estimated Primary Completion Date: April 2010 (Final data collection date for primary outcome measure)

Die aktuellen Daten kommen auf der Asco Anfang Juni. CDX 110 wird ein Erfolg werden, bereits mit Pfizer verpartnert, Celldex erhält für ein Approval 390 Millionen und natürlich ne Beteiligung am Umsatz. Denke Pfizer zielt auch auf den Nutzen in anderen Indikationen...aber dazu wird alles im Juni bekannt gegeben.

Überzeugt vom Erfolg CDX 110 hat mich folgendes

http://www.ariva.de/news/...ts-fuer-Patienten-mit-Hirntumoren-3258658

Aber Celldex hat mit CDX 011 (Brustkrebs, PH II), CRX 1307 (Blutkrebs PH1) und vielen präklinischen Antikörpern noch ein paar Eisen im Feuer. Schau mal in meinen Thread. Bin aktuell 58 % im Plus.

http://www.ariva.de/forum/...peutics-garantierte-100-bis-06-10-403476

und denke das Celldex bis auf 16 USd im Juni hochlaufen kann. Die letzten 2 Jahre gabs da immer ordentlich was zu holen.

Optionen

| Antwort einfügen |

| Boardmail an "Andreano" |

|

Wertpapier:

Dendreon

|

0

Optionen

| Antwort einfügen |

| Boardmail an "Magnetfeldfredy" |

|

Wertpapier:

Dendreon

|

1

Bei den Tests erhielten 82 Patienten das Arzneimittel, die bereits resistent gegenüber einer Hormontherapie waren. Zwar hemmte das Medikament den Krankheitsfortschritt, jedoch waren die Erfolge unbeträchtlich. Als Nebenwirkungen traten Erkältungen und Fieber auf.

Die Aktien fielen gestern an der NASDAQ um 0,99 Prozent und schlossen bei 2,00 Dollar.

da hat sich aber in 8 Jahren einiges getan....

Optionen

| Antwort einfügen |

| Boardmail an "Andreano" |

|

Wertpapier:

Dendreon

|

2

Ich wünsche Dir mit Celldex den Tenbagger den ich meiner ca. 10-jährigen Börsenkarriere mit allen Untiefen und Höhen erlebt habe, ein geiles Gefühl, das nur noch durch die Zulassung getopt werden könnte und dem Wissen, daß tausenden Prostatakrebskranken auf humane Weise geholfen werden kann!

Optionen

| Antwort einfügen |

| Boardmail an "Magnetfeldfredy" |

|

Wertpapier:

Dendreon

|

1

Mit ihren anderen Vaccines vorallem CDX 011 sind sie jetzt aber stärker in den Mittelpunkt gerückt, da zahlreiche Vaccines anderer Unternehmen in gleicher Indikation scheiterte.

Entweder sie vermarkten es alleine, davon geh ich momentan aus, denn Geld ist momentan noch ausreichend da, oder es kommt zu ner Übernahme.

Optionen

| Antwort einfügen |

| Boardmail an "Andreano" |

|

Wertpapier:

Dendreon

|

0

Provenge gehört zugelassen! Ohne wenn und aber... Dir viel Glück, erwarte den Tag mit Spannung

obwohl ich in DNDN nicht investiert bin.

Optionen

| Antwort einfügen |

| Boardmail an "Andreano" |

|

Wertpapier:

Dendreon

|

0

Optionen

| Antwort einfügen |

| Boardmail an "Magnetfeldfredy" |

|

Wertpapier:

Dendreon

|

0

Andreano, wird die Aktie hier diskutiert?

Ich finde es vorteilhaft wenn mehrere User sich beim Fakten zusammentragen unterstützen.

Das macht es mitunter leichter bei der Entscheidungsfindung, ersetzt selbstverständlich nicht die eigene Recherche.

Aber man sieht ja wie fleißig Magnetfeldfredy hier Infos reinstellt.

Optionen

| Antwort einfügen |

| Boardmail an "eyeonshare" |

|

Wertpapier:

Dendreon

|

0

vom letzten Jahr ASCO,

liefere die Tage noch einige Daten mehr...

Optionen

| Antwort einfügen |

| Boardmail an "Andreano" |

|

Wertpapier:

Dendreon

|

0

Optionen

| Antwort einfügen |

| Boardmail an "Andreano" |

|

Wertpapier:

Dendreon

|

1

Symbol: CLDX

Börse: NasdaqGM

WKN: A0RA0S

Aktueller Kurs: $6,86

Marktkapitalisierung: 217 Mio. USD

Ausstehende Aktien: ca. 32 Mio. Stück

Webseite: http://www.celldextherapeutics.com/

Kurze Zusammenfassung der Historie:

Celldex wurde 2004 als Spin-off der Biotechfirma Medarex gegründet. In 2007 fusionierte Celldex mit Avant Immunotherapeutics und ist seitdem an der Nasdaq gelistet.

Im Mai 2009 erwarb Celldex alle Anteile an der Biotechfirma CuraGen und somit 11 weitere Antikörper gegen Krebs.

Heute besitzt Celldex eine sehr umfangreiche Produktpipeline mit dem Schwerpunkt Krebsimpfstoffe.

Celldex ist zusammen mit Firmen wie Dendreon im erst kürzlich eingeführten Cancer Immunotherapy Index vertreten.

Nach Meinung vieler Experten gelten Immunotherapie und Krebsimpfstoffe als Krebstherapien der Zukunft.

Am 1. Mai wird die FDA mit allergrößter Wahrscheinlichkeit Provenge von der Firma Dendron als ersten Krebsimpfstoff für die Behandlung von Prostatakrebs zulassen.

Der Kurs von Dendreon hat sich mittlerweile vom Tief ausgesehen verzwanzigfacht, Dendreon wird heute bereits mit 5 Milliarden UDS bewertet.

Zukunftsorientierte Krebstherapien befassen sich mit der immunologischen Erkennung von Tumorzellen im Körper des Erkrankten. Diese Erkennung ist bei vielen Patienten nicht effektiv und begünstigt somit eine Ausbreitung der Erkrankung beziehungsweise ein Wiederauftreten der Erkrankung nach zunächst erfolgreicher Therapie.

Der Grundgedanke ist, das körpereigene Immunsystem zur Bekämpfung des Krebses heranzuziehen, und genau hier setzt Celldex mit seinen Produkten an.

Doch nun zur Pipeline von Celldex.

Bereich Cancer

1. CDX-110, Vaccine, Brain Cancer, Phase II

Das Produkt wird zusammen mit Pfizer entwicklet.

Pfizer hat eine Upfront-Zahlung in Höhe von 40 Mio. USD gezahlt und sich mit 10 Mio. USD an Celldex beteiligt.

Kommt es zur Zulassung kassiert Celldex weitere 390 Mio. USD an Meilensteinzahlungen. Nach Markteinführung zahlt Pfizer an Celldex eine zweistellige Royality-Rate bezogen auf den Umsatz.

Hier die Details zu dem Deal:

http://www.avance.ch/newsletter/docs/CelldexPfizer.pdf

Die bisherigen Ergebnisse zu CDX-110 waren sehr vielversprechend.

http://ir.celldextherapeutics.com/phoenix.zhtml?c=93243&p=ir…

Weitere Überlebensdaten werden möglicherweise auf der nächsten ASCO Anfang Juni präsentiert.

Das Umsatzpotential von CDX-110 gegen Gehirnkrebs wird weltweit auf ca. 1 Milliarde USD geschätzt. Bisher eingesetzte Therapien wirken kaum.

CDX-110 hat zusätzlich das Potential auch bei anderen Krebsarten zu wirken.

2. CDX-011, Antibody Vaccine, Breast Cancer, Phase II

Auch hier waren die bisher vorgelegten Studenergebnisse sehr vielversprechend.

http://ir.celldextherapeutics.com/phoenix.zhtml?c=93243&p=ir…

Dazu gibt es auch noch einen sehr interessanten Artikel.

http://seekingalpha.com/article/147378-curagen-positive-resu…

3. CDX-011, Antibody Vaccine, Melanoma, Phase II

Aktuelle Ergebnisse werden auf der nächsten ASCO Anfang Juni präsentiert.

4. CDX-1307, Antibody Vaccine, Bladder Cancer, Phase I

Auch hier liegen erste positive Studienergebnisse vor.

http://ir.celldextherapeutics.com/phoenix.zhtml?c=93243&p=ir…

Der Start der Phase 2 ist in Kürze zu erwarten.

5. CDX-1401, Antibody Vaccine, Multiple Tumors, Phase I

http://ir.celldextherapeutics.com/phoenix.zhtml?c=93243&p=ir…

6. CDX-1127, Antibody Vaccine, Cancer, Preclinical

Präsentation am 21. April.

http://www.abstractsonline.com/Plan/ViewAbstract.aspx?sKey=4…

Neben den Krebsimpfstoffen ist Celldex noch auf zwei weiteren Gebieten tätig. Infos dazu findet ihr auf der webpage von celldex.

Inflammatory diseases

7. CDX-1189, Antibody, Renal disease, Preclinical

8. CDX-1135, Soluble receptor, Renal disease, Preclinical

Infectious diseases

9. ColeraGarde, Vaccine, Enteric diseases, Phase II

10. ETEC, Vaccine, Enteric diseases, Phase II

11. Tyo 800, Vaccine, Typhoid fever, Phase II

12. CDX-2401, Antibody Vaccine, HIV infection, Preclinical

Hier die nächten Meilestones kopiert von der Celldex webpage:

In 2010, we plan to:

Report final Phase 1/2 data from a clinical study of CDX-011 in patients with advanced melanoma at the American Society of Clinical Oncology (ASCO) conference in June.

Report additional results from the Phase 1 clinical study of CDX-1307 in patients with advanced epithelial cancers, including breast, colon and pancreatic cancer at the ASCO conference in June.

Report preliminary data from the Phase 1/2 clinical study of CDX-1401 in patients with malignant solid tumors that express NY-ESO-1.

Initiate a randomized Phase 2b clinical study of CDX-1307 in combination with immune modulators in patients with muscle-invasive bladder cancer expressing hCG-beta.

Initiate an expanded Phase 2b clinical study of CDX-011 in patients with GPNMB-expressing breast cancer including triple negative disease.

Die ASCO dürfte somit sehr spannend werden.

Die Übernahme durch einen der großen Player ist auch jederzeit möglich.

Abschließen noch ein link zu einer aktuellen Firmenpräsenatation:

http://ir.celldextherapeutics.com/phoenix.zhtml?c=93243&p=ir…

Fazit

Investitionen in Biotechunternehmen, die wie Celldex, noch keinen Umsatz erwirtschaften sind sehr riskant, da das Scheitern eines Produktes mit einem signifikanten Kursverfall einhergeht.

Andererseits winken bei erfolgreichen Produktzulassungen enorme Kurssteigerungen.

Celldex ist mit seiner pipeline (12 Produkte) breit aufgestellt und bewegt sich mit der Fokusierung auf Krebsimpfstoffe in einem vielversprechenden Zukunftsmarkt.

Die Kooperation mit Pfizer zeigt, dass die großen Player Interesse an der pipeline von Celldex haben.

Der aktuelle cash von Celldex (ca. 55 Mio. USD) reicht noch für ca. 2 Jahre.

Ist CDX-110 weiterhin erfolgreich fließen weitere Millionen von Pfizer zu.

Insgesamt meiner Meinung nach ein gutes Chance/Risiko Profil.

Optionen

| Antwort einfügen |

| Boardmail an "Andreano" |

|

Wertpapier:

Dendreon

|

2

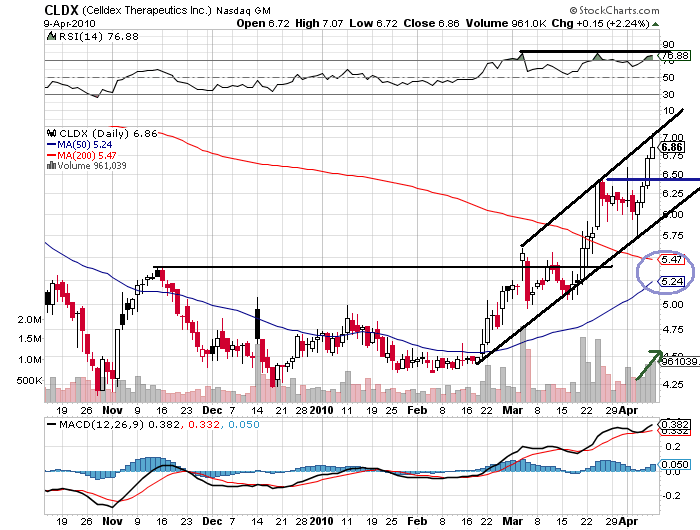

die Trading-Range ist nach oben hin ausgereizt, rechne mit Rückgang bis auf 6,50 USD

wer einsteige will, sollte da zuschlagen

MA(50) kreuzt bald MA(200) dann wirds interessant, rechne zu dem Zeitpunkt mit nem mächtigen Schub, die Amis fahren auf die Charttechnik ab...vorallem in kleineren Werten

Optionen

| Antwort einfügen |

| Boardmail an "Andreano" |

|

Wertpapier:

Dendreon

|

Angehängte Grafik:

sc.png (verkleinert auf 72%)

sc.png (verkleinert auf 72%)

3

Analyst Sees FDA Approval For Provenge Drug By Dendreon (DNDN); Upgrades Stock To Buy Rating

Buzz up! 0 Print

Companies:Amgen Inc.Dendreon Corp.Human Genome Sciences Inc. Related Quotes

Symbol Price Change

AMGN 60.51 -0.39

DNDN 39.26 -0.13

HGSI 32.82 -0.04

LIFE 51.73 -0.62

{"s" : "amgn,dndn,hgsi,life","k" : "c10,l10,p20,t10","o" : "","j" : ""} On Monday April 12, 2010, 10:43 am

67 WALL STREET, New York - April 12, 2010 - The Wall Street Transcript has just published its Biotechnology & Pharmaceuticals Report offering a timely review of the sector to serious investors and industry executives. This 36 page feature contains expert industry commentary through in-depth interviews with public company CEOs, Equity Analysts and Money Managers. The full issue is available by calling (212) 952-7433 or via The Wall Street Transcript Online.

Topics covered: Clinical, Financial & Regulatory Risks To Drug Development - Easing Capital Markets - Managing Inherent Volatility - FDA Approval Process - Small- & Mid-Cap M&A Rally - Basket Investment Approach - Impact Of Health Care Reform - Therapeutic Cardiovascular Plays - Investable Trend In Antibody Technology

Companies include: Genentech/Roche (RHHBY); Medivation (MDVN); Seattle Genetics (SGEN); AEterna Zentaris (AEZS); Abbott (ABT); Alexion (ALXN); Amgen (AMGN); Antares Pharmaceuticals (AIS); Ardea (RDEA); Astellas (4503); AstraZeneca (AZN); Auxilium (AUXL); Biogen (BIIB); CardioGenics (CHNG); Celera (CRA); Celgene (CELG); Celldex (CLDX); and many more.

In the following brief excerpt from the 36 page , interviewees discuss the outlook for the sector and for investors.

Dr. Jonathan Aschoff, Ph.D., is a Senior Equity Analyst at Brean Murray, Carret & Co., LLC. Prior to joining the firm in 2003, he held positions as a Senior Biotechnology Analyst at Friedman, Billings, Ramsey & Co., Inc., and at what is now RBC. He also served as an Analyst at Sturza Institutional Research. Prior to Wall Street, Dr. Aschoff was a Research Technician at New England Medical Center. He earned a Ph.D. in molecular biology and microbiology, as well as a B.S. in biology from Tufts University.

TWST: Let's start with Medivation (MDVN). Why did you have a "sell" rating on it when most analysts had it as a "buy"-rated stock?

Dr. Aschoff: I had absolutely no belief that the heterogeneous European, American and South American patient population in Medivation's Phase III trial that just failed could ever replicate the homogeneous group of Russian patients that were largely recruited at only three of 11 sites in the Russian trial - that was the original Alzheimer's trial for Dimebon. Everything about the company was difficult to trust and partner Pfizer (PFE) has made many bad investments, so that deal had no chance of scaring me away.

TWST: What about Dendreon? You had a "sell" rating for five years and now you have a "buy" rating. What happened?

Dr. Aschoff: They put up solid data early in 2009. I think the thing to learn from Dendreon (DNDN) is when a stock is essentially at an all-time low going into a pivotal event, you might want to back off from being so aggressive with a "sell" rating. You might have wanted to consider that hardly anyone favored it then, so how much lower could it go? I was able to see the data presented in Chicago last year, and then my last concern of stroke imbalance, which was an imbalance in the first two Phase III trials, was assuaged when there was no imbalance in the IMPACT trial.

The trial arms were perfectly balanced, 6-3 for a 2-1 randomized trial. So I had no safety concerns, and that's when I went from the "hold" rating that I went to about a week before to a "buy" rating at about $20 per share, and it has been almost a double from there. I don't see anything getting in the way of FDA approval for Provenge. Approval would be a material risk reduction that would justify the stock to be well into the $40s because now you have removed FDA risk and Dendreon now just has to commercialize it, which they have enough money to do smoothly, and to train the employees properly.

TWST: How important to you is company management?

Dr. Aschoff: The earlier the assets, the less I care. But it matters more when it comes to commercializing something, and then I care more. Early on it is only about what the drug does, and that's in the hands of the patients and the people at the clinical trial sites. Management then gets more involved as you get into writing up the application efficiently and considering if management is likely to give a good retort to anything that might be argued against them at an FDA panel. Are they now likely to get a partner on good terms? Can they actually sell this treatment alone or with a partner? That's really what brings more to bear on management. The pivotal data, relatively speaking, is more out of their hands.

TWST: Must small biotechs always have a partnership somewhere down the road?

Dr. Aschoff: No, they don't have to. Good data will beget that if it makes sense to have a partner, and so they don't have to. I mean, I like Ardea (RDEA), Dendreon, Alexion (ALXN) and United Therapeutics (UTHR) a lot, and they don't have large pharmaceutical partners.

TWST: Why do you like Ardea?

Dr. Aschoff: Because by the time this interview is published, I think you are going to get a very positive Phase IIb monotherapy result. The bears think Ardea's drug is unsafe; they think it works, but that it's unsafe. I think it works, I agree with them on that, and I think it's safe. I don't think you are going to have kidney complications - that's the whole argument. I cover a lot of battle ground stocks and RDEA is one of them. Their monotherapy Phase IIb data should look good and so should their combination therapy data in April. And so we have imminent catalysts, which is why I launched coverage in December. I expect positive Phase IIb data to beget acquisition of the company.

The Wall Street Transcript is a unique service for investors and industry researchers - providing fresh commentary and insight through verbatim interviews with CEOs and research analysts. This 36 page special issue is available by calling (212) 952-7433 or via The Wall Street Transcript Online .

The Wall Street Transcript does not endorse the views of any interviewees nor does it make stock recommendations.

For Information on subscribing to The Wall Street Transcript, please call 800/246-7673

Buzz up! 0 SendSharePrintShare this page

DeliciousTwitterMyspaceDiggStumbleUponFacebook

Optionen

| Antwort einfügen |

| Boardmail an "Magnetfeldfredy" |

|

Wertpapier:

Dendreon

|

0

Celldex wird in 1-2 Tagen ausbrechen _Chart Analyse

( http://www.ariva.de/forum/...eutics-garantierte-100-bis-06-10-403476)

und News http://www.fool.com/investing/small-cap/2010/04/...ng-the-market.aspx

Dendreon dümpelt so vor sich hin, wird Zeit, dass die Zulassung kommt (wo seht ihr den Kurs eigentlich dann?)

Optionen

| Antwort einfügen |

| Boardmail an "Andreano" |

|

Wertpapier:

Dendreon

|

0

Optionen

| Antwort einfügen |

| Boardmail an "Andreano" |

|

Wertpapier:

Dendreon

|

0

Re: Citibank downgrades to Hold; increases target from $35 to $40

Optionen

| Antwort einfügen |

| Boardmail an "Magnetfeldfredy" |

|

Wertpapier:

Dendreon

|

0

PROVENGE Significantly Prolongs Survival in Men with Advanced Prostate Cancer in Pivotal Phase 3 IMPACT Study

– Study Meets Primary Endpoint Showing Statistically Significant Improvement in Overall Survival –

– First Active Immunotherapy for Cancer to Prolong Survival –

– Full Data to be Presented at Plenary Session at Upcoming AUA Annual Meeting –

– Company to Host a Conference Call Today at 9:00 AM ET –

SEATTLE, April 14, 2009 - Dendreon Corporation (Nasdaq: DNDN) announced today that the pivotal Phase 3 IMPACT study of PROVENGE® (sipuleucel-T) in men with advanced prostate cancer met its primary endpoint of improving overall survival compared to a placebo control. The magnitude of the survival difference observed in the intent to treat population resulted in the study successfully achieving the pre-specified level of statistical significance defined by the study's design. The safety profile of PROVENGE appeared to be consistent with prior trials.

The 512-patient, multi-center, randomized, double-blind, placebo-controlled IMPACT (IMmunotherapy for Prostate AdenoCarcinoma Treatment) study enrolled men with metastatic androgen-independent prostate cancer was conducted under a Special Protocol Assessment agreement with the U.S. Food and Drug Administration (FDA).

PROVENGE is Dendreon's investigational product candidate for men with advanced prostate cancer and may represent the first in a new class of active cellular immunotherapies specifically designed to engage the patient's own immune system against cancer.

Detailed results from the IMPACT study will be presented during a plenary session at the American Urological Association's Annual Meeting in Chicago on Tues., Apr. 28 at 2:20 pm CT.

"Survival is the gold standard outcome for oncology clinical trials, and overall survival was the primary endpoint of the IMPACT trial. The positive results from this landmark study provide confirmatory evidence demonstrating that treatment with PROVENGE may prolong survival," said Mitchell H. Gold, M.D., president and chief executive officer of Dendreon. "We are immensely grateful to our clinical investigators and the more than 1,000 men with advanced prostate cancer who have participated in our studies over the last decade and whose courage and contribution have significantly advanced the understanding and treatment of prostate cancer and the potential role of cancer immunotherapies."

"The successful outcome from the Phase 3 IMPACT study provides validation of the long-pursued goal of harnessing the human immune system against a patient's own cancer," continued Dr. Gold.

Because the data meet the criteria and specifications outlined in its Special Protocol Assessment (SPA) agreement with the FDA, Dendreon intends to file an amendment to its existing Biologic License Application (BLA) in the fourth quarter of this year to gain licensure of PROVENGE.

Prostate cancer is the most common non-skin cancer in the United States and the third most common cancer worldwide. More than one million men in the United States have prostate cancer, with an estimated 186,320 new cases and approximately 28,660 men who were expected to die from the disease in 2008. Currently there are limited treatment options for men with advanced, metastatic prostate cancer.

Conference Call Scheduled for Today at 9:00 a.m. ET

Dendreon will host a conference call today at 9:00 a.m. ET. To access the live call, dial 1-877-419-6594 (domestic) or 719-325-4855 (international). The call will also be audio webcast and will be available from the Company's website at www.dendreon.com under the "Investor/Webcasts and Presentations" section. A recorded rebroadcast will be available for interested parties unable to participate in the live conference call by dialing 1-888-203-1112 (domestic) or 719-457-0820 (international); the conference ID number is 8182435. The replay will be available from 12:00 p.m. ET on April 14, 2009 until midnight April 16, 2009. In addition, the webcast will be archived for on-demand listening for 30 days at www.dendreon.com.

About PROVENGE

PROVENGE ® (sipuleucel-T), an investigational product in development for men with androgen-independent prostate cancer, may represent the first product in a new class of active cellular immunotherapies (ACIs). PROVENGE and other ACIs are uniquely designed to use live human cells to engage the patient's own immune system with the goal of eliciting a specific long-lasting response against cancer. In controlled clinical trials, the most common adverse events were chills, fever, headache, fatigue, shortness of breath, vomiting and tremor. These events were primarily low grade with a short duration of 1-2 days following infusion.

Optionen

| Antwort einfügen |

| Boardmail an "Magnetfeldfredy" |

|

Wertpapier:

Dendreon

|

0

GO DNDN, GO CLDX

Optionen

| Antwort einfügen |

| Boardmail an "Andreano" |

|

Wertpapier:

Dendreon

|